The Hard Forks That Didn’t Dilute Bitcoin – CoinDesk

Some time ago, one of the more thoughtful critiques of Bitcoin went a little like this:

“Sure, bitcoin is scarce in its supply, but since it’s effectively costless to clone the software and fork it, it’s not scarce overall. Forks constitute effective dilution and render the Bitcoin system’s commitment to a hard cap irrelevant.”

This wasn’t altogether a terrible point. For a moment in 2017, it seemed like Bitcoin was being forked on a weekly basis. I’ll confess to feeling a twinge of concern when bitcoin cash (BCH) launched on Coinbase at $4,000 and it seemed like a genuine possibility that it might surpass bitcoin. One of Bitcoin’s peculiarities is the fact that anyone can costlessly replicate its UTXO set and claim affiliation to the original chain. Some particularly confident promoters have even gone as far as to claim their forks actually constitute the original Bitcoin, with the legacy chain being the imposter.

If any of these forks had meaningfully gained ground relative to Bitcoin, the critics would have had a point. What’s the point of a monetary network which is undergoing a constant state of fragmentation?

CoinDesk columnist Nic Carter is partner at Castle Island Ventures, a public blockchain-focused venture fund based in Cambridge, Mass. He is also the cofounder of Coin Metrics, a blockchain analytics startup.

I was reminded of this concern by MicroStrategy CEO Michael Saylor in his recent appearance on Anthony Pompliano’s podcast. Saylor, the first public company CEO to allocate a meaningful portion of his company’s balance sheet to Bitcoin, had this to say:

The hard forks I think are a big advantage. The fact that Bitcoin went through it and we saw what happened and we saw that the community would defend Bitcoin, that’s what gives a person like me confidence to invest hundreds of millions of dollars into bitcoin. I don’t want to hear that you have got a new idea and you are upset over transaction fees and you would like to implement smart contracts and change everything. […] I want to hear that you are going to defend the network to the death against someone that is going to break it or compromise it in any way shape or form.

With the benefit of hindsight, it’s now clear the challenger forks have been completely rejected. This wasn’t something that was evident in 2017, and it’s indicative of bitcoin’s continued maturation as a monetary asset of consequence.

There are many ways to measure the salience of forks, but the simplest is their aggregate economic significance. When you adjust for free float (as in, taking into account only units which are actually circulating), BCH amounts to a meager 1.7% of bitcoin’s market capitalization, an all-time low since inception. Bitcoin sv (BSV) accounts for a measly 1%.

Transaction fees, used to guarantee the sustainability of miner revenue and hence network security in the long term, are robust in bitcoin (>$700k daily) and practically nonexistent in BCH and BSV ($137/day and $73/day over the last week, respectively). If they can’t muster demand for their blockspace – and I don’t see any catalysts to reverse this trend – they will be forced to reintroduce inflation, centralize block signing, or devise some new consensus mechanism.

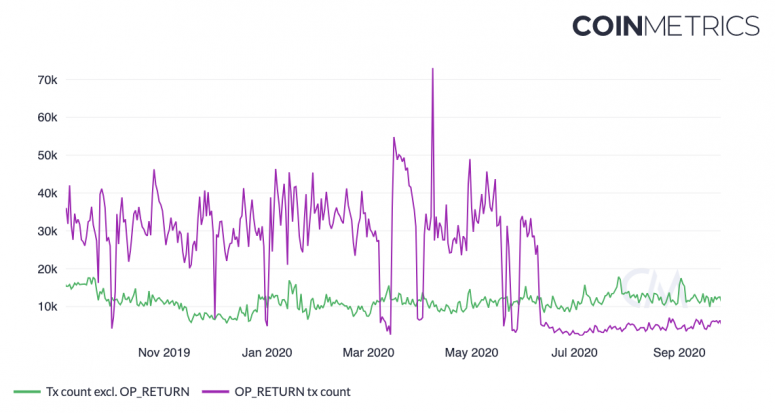

And if you eliminate non-monetary OP_RETURN transactions (used to insert arbitrary data into blockchain), Bitcoin Cash settles about 12,000 transactions a day, compared to Bitcoin’s ~350,000.

For a network whose foundational value proposition involved vastly increasing the supply of blockspace to pursue the low-fee, peer-to-peer petty cash vision of Bitcoin, this is a considerable letdown. Three years on, the core hypothesis of Bitcoin Cash – that cheaper blockspace would be more amenable to vibrant on-chain commerce – looks more remote than ever. How long must enthusiasts defer their dream before they admit that a minority, largely undifferentiated clone of Bitcoin isn’t a particularly compelling proposition?

Today, BCH is facing an insurrection and yet another hard fork due to an inability to finance its core developers. Unlike Bitcoin, it never developed a meaningful patronage system. So now certain BCH developers are holding the chain hostage and demanding that miners be expropriated to subsidize their work. The looming hard fork is a consequence of founding the chain on a secessionist impulse. If your reaction to disputes is to fork the chain rather than resolve them, you are likely condemning yourself to a litany of future forks.

By refusing to compromise on its key features, Bitcoin has retained its luster while avoiding capture.

All of this bodes poorly for future minority forks. Investors tend to fight the last war. As BCH, BSV and other more marginal forks fade into irrelevance, they will be very wary of any newer protest forks.

Back in 2017, it was popular to proclaim that Bitcoin, and other cryptocurrencies, were governed by the possibility of exit. If users and investors disagreed with the direction of the project, they could simply fork it and build something more to their liking, or so the saying went. This always rankled me because the natural end state of this paradigm – if taken to its logical conclusion – would be a hopeless fragmentation of Bitcoin’s user base into dozens of marginally different tribes.

This seems unacceptable. Bitcoin is designed such that users agree over a very narrow set of principles, in order to obtain global convergence on a UTXO set. The smaller the argument space, the less likely the project is riven by irreconcilable differences between users. By refusing to compromise on its key features, Bitcoin has retained its luster while avoiding capture.

See also: Nic Carter – The Biggest Story in Crypto: The Stablecoin Surge and Power Politics (podcast)

Interestingly, it’s this inflexibility that permits it to appeal to a heterogeneous user base. Bitcoin users do not need to believe in anything other than the merit of a sound, finite supply, fast-settling digital money system. As Saylor notes, far from being a drawback, Bitcoin’s rigidity is a source of strength and credibility. We’re talking about monetary goods here: something you’d feel confident allocating your savings to for decades. Bitcoin’s stewards don’t take this task lightly, and it shows.

It’s clear now that Bitcoin’s network-driven advantages are insurmountable. If Bitcoin were to be supplanted as a digitally native sound money, its challenger would have to be radically different, with dramatic 10x improvements in multiple key domains. Bitcoin is by no means guaranteed to win as the internet’s sole sound money. But at the very least, we can put one old critique to bed.

Note: the caption on the second chart here has been corrected.